The Real Question Is Not “Can I Move My UK Pension?”

For many US residents with UK private pension assets, the first question is often framed too narrowly: can I move my UK pension?

That is rarely the right starting point.

A UK pension does not become a US retirement account because its member becomes US-resident. It remains a UK pension, governed by UK pension legislation, HMRC rules, scheme documentation, trustee or provider discretion, and UK regulatory constraints. What changes is the surrounding planning environment.

Once the pension holder is within the US tax system, the pension may become relevant for US federal income tax, state tax, treaty analysis, foreign asset reporting, investment implementation, estate planning and family succession. The pension’s legal identity may remain British, but the consequences of holding, accessing, transferring or leaving it to beneficiaries may become substantially more complex.

The planning question is therefore not simply:

Can my UK pension be transferred?

It is:

How should my UK pension be governed, reported, accessed, invested and ultimately distributed within a US tax, treaty and family-wealth context?

That distinction matters. For US residents, transferring a UK pension outside the UK is rarely the optimal outcome and, in practice, is usually the wrong solution to the problem being considered. UK pensions are highly regulated retirement structures with established tax, governance and beneficiary frameworks. In many cases, they remain among the most valuable long-term planning vehicles available to internationally mobile families.

There are specialist UK pension arrangements and providers that are accustomed to servicing US-resident members, accommodating US tax considerations and cross-border reporting requirements without requiring the pension itself to leave the UK. As a result, the planning exercise is often not about moving the pension, but about ensuring the existing pension is held in an appropriate structure, with suitable investment implementation and beneficiary arrangements.

It is also important to distinguish between a pension transfer and a pension withdrawal. A direct transfer from a UK pension into a US-qualified retirement account such as an IRA or 401(k) is generally not available under either UK pension law or US retirement-plan rules. In practical terms, the only way assets move from a UK pension into a US retirement account is usually by first taking a taxable distribution from the UK pension and then making a separate contribution to the US arrangement, subject to the normal US contribution limits and eligibility requirements. For most affluent clients, this is neither an efficient nor a commercially compelling strategy.

Accordingly, the default assumption should generally be that a UK pension remains in the UK unless there is a specific and well-supported reason to consider an alternative. The burden of proof typically rests with the transfer proposal, not with retaining the pension. Drawing benefits may be appropriate where liquidity, retirement income, estate planning or tax timing objectives justify access, but those decisions should be made within a coordinated UK-US framework rather than as part of an attempt to replicate a US retirement account structure.

For internationally mobile families, the pension is rarely an isolated asset. It may sit alongside US employment income, UK property, carried interest, restricted stock units, business sale proceeds, trusts, non-US beneficiaries, a green card decision, or a future move away from the United States. In those cases, the pension decision is not a product decision. It is a cross-border balance-sheet decision.

Can a US resident keep a UK pension?

Yes. A UK pension can continue to be held after the member becomes US-resident. US residence does not, by itself, force a UK pension to be transferred, surrendered or collapsed. The scheme remains subject to UK pension rules, including access age, authorised payment rules, provider terms and transfer restrictions.

But “can I keep it?” is only the first layer of the analysis. A US-resident holder must also consider how the pension is treated for US tax purposes, whether treaty relief applies, what reporting may be required, how withdrawals are characterised, whether the provider can continue servicing the member, and how death benefits will be treated if the member dies while US-resident.

The UK-US tax treaty is central, but it is not a complete answer. HMRC’s Double Taxation Relief Manual explains the treaty framework for pensions under Articles 17 and 18, including the distinction between pension income, lump sums, scheme earnings and contribution relief. However, the treaty operates alongside US domestic law, the treaty saving clause and US reporting rules. It does not convert a UK pension into an IRA, 401(k), Roth IRA or other US-qualified retirement arrangement.

This is where many poor decisions begin. A client hears that the pension remains UK-recognised. Or that the treaty covers pensions. Or that QROPS is available. Each statement may be partly true. None is sufficient.

Different pension events may have different consequences. An intact pension, periodic drawdown, a pension commencement lump sum, a UK-to-UK transfer, a third-country QROPS transfer and a death benefit payment should not be assumed to have the same US tax, reporting or treaty treatment.

IRS administrative guidance is particularly important here. In AM2008-009, the IRS Office of Chief Counsel concluded that Article 18 of the UK-US tax treaty does not override the normal US rules governing retirement-plan rollovers. In practical terms, this means that a distribution from a UK pension cannot automatically be transferred into a US retirement account on a tax-deferred basis simply because the treaty applies. The transaction must still satisfy the relevant US domestic rollover requirements.

Lump sums require similar care. The UK may treat part of a pension commencement lump sum as tax-free, but that does not automatically settle the US answer. IRS INFO 2008-0024 addressed a UK pension lump sum and explained that the treaty saving clause may preserve the United States’ ability to tax a US resident, even where the relevant treaty article would otherwise appear to allocate taxing rights differently.

A US-resident individual cannot assume that the familiar UK rule allowing up to 25% of pension benefits to be taken tax-free will produce the same outcome for US tax purposes. A UK pension commencement lump sum may be treated differently in the United States, depending on factors such as citizenship, treaty position, contribution history and pension basis. For higher-net-worth families, advance planning is essential, as timing, residency, foreign tax credits, state taxes and withdrawal sequencing can materially affect the tax outcome.

Hence, the practical implication is straightforward: the pension should be mapped before it is moved, drawn or restructured. The relevant review normally includes residence status, citizenship or green card position, treaty residence, pension type, contribution history, prior transfers, beneficiary nominations, reporting exposure, investment implementation, state tax and future mobility.

For internationally mobile clients, the first step is usually not a pension product decision. It is a structured review of residence, treaty position, pension type, reporting exposure, beneficiary design and future mobility.

This article sets out the governing framework. It explains why a UK pension is not automatically treated like a US retirement account, how the UK-US treaty should be approached, why transfer and QROPS analysis require caution, and which access, investment and family issues often determine the appropriate course.

2. The Common Misconception: A UK Pension Is Not Automatically Treated Like an IRA or 401(k)

The most common misconception is that a UK pension will be treated in the United States as though it were broadly equivalent to an IRA, 401(k), Roth IRA or another US-qualified retirement plan.

That assumption is unsafe.

A UK pension may be fully recognised and tax-advantaged in the United Kingdom while still raising separate questions under US tax law. HMRC recognition does not mean IRS approval. A UK pension wrapper does not automatically import US-qualified plan treatment. Nor does UK tax deferral necessarily mean that the United States will treat every contribution, investment return, withdrawal, transfer or beneficiary payment in the same way.

This point is often underestimated. Many US residents, including sophisticated investors with UK pensions, seek clarification directly from the IRS, only to receive informal guidance that may be incomplete, inconsistent or incorrect. Cross-border pension treatment is determined by legislation, treaty provisions and published administrative guidance rather than telephone conversations. For significant withdrawals, transfers, consolidations or retirement-planning decisions, specialist cross-border advice is often prudent before taking action, particularly where US tax, treaty and reporting considerations may materially affect the outcome.

I would encourage you to arrange a confidential cross-border pension review with ourselves at Harrison Brook before making any irreversible decisions. For US residents holding UK pension assets, a thoughtful and structured assessment can provide clarity on treaty treatment, US reporting obligations, withdrawal strategy, transfer considerations and longer-term family planning.

The distinction between a pension being recognised under UK pension law and being treated as a US-qualified retirement arrangement for US tax purposes is more than a matter of terminology. It can influence when income is recognised for US tax purposes, whether treaty relief is available, whether a treaty-based filing position should be disclosed, whether a transfer is treated as taxable, whether foreign account or asset reporting obligations arise, and ultimately whether beneficiaries inherit a well-structured asset or a complex cross-border issue requiring resolution.

For US-connected clients, the relevant question is not “is this pension in the UK?” The better question is:

How is this arrangement treated in the US for tax, treaty, reporting and estate-planning purposes, and what changes if I access, transfer or die holding it?

The answer may depend on the scheme type, contribution history, residence profile, citizenship and domicile, transfer destination, reporting classification, beneficiary structure and the form in which benefits are eventually taken.

A UK defined contribution pension, SIPP, occupational defined contribution plan, defined benefit scheme, historic employer pension, UK-to-UK consolidated arrangement or prior overseas transfer may each require a different analysis. The same pension may also produce different answers depending on whether the holder is a US citizen, green card holder, long-term resident alien, temporary assignee, dual resident, or a non-US citizen living in a state with its own tax treatment.

The important point is not that UK pensions are inherently unattractive for US residents. They are not. In most cases, keeping your UK pension is entirely rational, and likely the best course of action. The point is that the US treatment must be built from the facts, and not inferred from the UK label.

Why UK Pension Status Alone Does Not Determine the US Outcome

It is correct to say that a UK pension remains a UK pension after the member moves to the United States. UK pension law still matters. HMRC rules still matter. Scheme rules, provider terms, trustee discretion and UK authorised payment rules still matter.

But that does not answer the US question.

For US purposes, the analysis should involve domestic income tax rules, the UK-US treaty, the treaty saving clause, foreign pension distribution rules, foreign trust reporting concepts, foreign financial asset reporting and the legal architecture of the specific arrangement.

The IRS guidance on foreign pension and annuity distributions makes clear that foreign pension payments may be taxable in the United States even where the taxpayer does not receive the familiar US information slips associated with domestic retirement plans. In broad terms, the taxable amount often turns on the gross distribution less the taxpayer’s cost or investment in the contract, which can make historic contribution records important for older UK schemes.

In simpler terms, many people assume that if a UK pension payment arrives in their bank account, the amount received is either fully taxable or fully tax-free. The US rules are often more nuanced. Part of a payment may represent contributions that have already been taxed at some point, while another part may represent investment growth or employer-funded benefits that could be taxable when withdrawn. This is one reason why keeping records of contributions, transfers and pension statements can be valuable, particularly for long-established UK pensions where the history may stretch back decades; obtaining coordinated advice from a UK-US cross-border financial planner and tax adviser can also be invaluable when reconstructing contribution history and determining the correct US tax treatment.

That is particularly relevant for clients with long contribution histories, employer-funded schemes, historic transfers, partial withdrawals or incomplete records. In practice, basis reconstruction can become a material planning exercise, not an administrative footnote.

The US analysis may also differ depending on the event. An intact UK pension that has not yet been accessed raises one set of questions. Periodic income raises another. A UK pension commencement lump sum raises another. A UK-to-UK transfer may need to be distinguished from a transfer to a third-country Qualifying Recognised Overseas Pension Scheme (QROPS). A death benefit paid to a surviving spouse, adult child, trust or non-US beneficiary may require still further analysis.

This is why broad labels can mislead. “It is still a UK pension” is relevant, but incomplete. “It is HMRC-recognised” is useful, but not determinative. “It is tax-free in the UK” may be correct for a particular UK event, but it does not automatically answer the US tax question.

A more disciplined approach is to separate the UK-side fact from the US-side planning question.

| UK-side fact | US-side question | Why it matters |

| UK pension remains intact | Is there US reporting, foreign asset disclosure or annual tax relevance while no UK benefit is being taken? | A pension can create review points before any withdrawal occurs. |

| Periodic income begins | Is the payment taxable in the US, protected by treaty, subject to UK withholding, or affected by state tax? | Cash flow, withholding and reporting may need to be coordinated. |

| 25% pension commencement lump sum is taken | Does UK tax-free treatment carry across to the United States? | UK tax-free cash is one of the most frequent sources of incorrect US assumptions. |

| UK-to-UK transfer | Is the movement merely an internal UK pension event, or does it create US tax or reporting consequences? | Consolidation may be sensible, but US classification should be checked before action. |

| UK-to-third-country QROPS transfer | Is the receiving scheme protected, reportable, taxable or outside expected treaty treatment? | UK transfer permission is not the same as US tax acceptance. |

| Beneficiary or death benefit event | How do UK pension rules, US estate tax, UK inheritance tax, beneficiary residence and nominations interact? | Family outcomes may depend on more than the pension nomination form. |

This framework is also why should be read before assuming that a transfer solves the problem. IRS INFO 2011-0096 is important because it distinguishes a UK-to-UK pension transfer from a transfer to a third-country pension scheme. It notes that a third-country arrangement may fall outside the UK-US treaty definition of a pension scheme and could be treated as a taxable distribution for US purposes.

Why the UK-US Tax Treaty Alone Is Not Enough for UK Pension Planning in the United States

The UK-US tax treaty is an essential part of the analysis. It is not a universal answer.

Treaties allocate taxing rights and provide relief mechanisms in defined circumstances. They do not rewrite every part of domestic law. They do not automatically turn a UK pension into a US-qualified retirement account. They do not create a general rollover pathway into an IRA or 401(k). They do not eliminate reporting, disclosure, state tax, transfer risk or the need to characterise the pension event correctly.

The treaty saving clause is particularly important. In broad terms, it can preserve US taxing rights over US citizens and, in certain cases, US residents, even where a treaty article appears to provide relief. HMRC’s own treaty manual highlights this issue in the context of UK pension lump sums, noting that Article 17(2) is not among the provisions exempted from the saving clause. IRS INFO 2008-0024 reaches the same practical conclusion for a US resident receiving a UK pension lump sum.

Treaty relief may also depend on correct filing positions. In some cases, a taxpayer may need to disclose a treaty-based return position, commonly through Form 8833. In others, the relevant question is not whether the treaty exists, but whether the taxpayer’s pension type, residence status, citizenship, distribution form and transaction history fall within the protection being claimed.

Reporting should not be treated as a clerical afterthought. Depending on the pension structure and the taxpayer’s wider facts, review points may include Form 8938, FBAR, Forms 3520 and 3520-A, Form 8833, and in some cases reportable transaction analysis. Rev. Proc. 2020-17 may provide relief for certain tax-favoured foreign retirement trusts, but it is not a blanket exemption for every UK pension arrangement, and it does not eliminate all foreign financial asset or foreign account reporting questions.

This is where many simplified explanations fail. They identify a treaty article, then stop. Serious planning cannot stop there.

In my own work advising internationally mobile families, entrepreneurs and executives, I have encountered a wide range of approaches to UK pension reporting among US residents. Some individuals have been advised that no reporting was required. Others have simply assumed that because the pension remained in the UK, it fell outside the scope of US disclosure obligations. In certain cases, the position ultimately proved acceptable based on the specific facts and the applicable rules. In others, it did not.

That experience is not unusual within the cross-border advisory industry. UK pensions occupy an area where treaty provisions, domestic tax rules, reporting requirements and administrative guidance intersect, and misunderstandings are common. The fact that different advisers may reach different conclusions on particular reporting questions does not remove the need for a careful, evidence-based analysis.

As advisers, our role is to explain the applicable rules, identify risks, document reasonable positions and help clients remain compliant with their legal obligations. We cannot compel a client to adopt a particular filing position, nor can we assume responsibility for decisions ultimately taken on a tax return. Equally, no responsible adviser should encourage under-reporting, non-disclosure or aggressive interpretations that cannot be properly supported.

The practical lesson is straightforward. Where there is uncertainty, it is generally preferable to investigate the issue before filing rather than assume that a UK pension can be ignored for US tax or reporting purposes. The cost of obtaining clarity is often modest compared with the potential consequences of discovering years later that a pension, transfer, distribution or reporting obligation was misunderstood. For most internationally mobile families, a cautious and well-documented approach is usually the more prudent course.

For a US resident with UK pension assets, the treaty analysis should be integrated with the wider facts: the type of pension, where it was established, whether contributions were made before or after US residence began, whether benefits are being taken as income or lump sum, whether a transfer is being considered, whether the member is a US citizen or green card holder, and whether the relevant state follows or departs from the federal treatment.

The practical conclusion is deliberately cautious: the treaty matters, but it is not enough on its own. It should be read alongside US domestic rules, UK pension rules, scheme documentation, reporting obligations, investment implementation and the family’s broader objectives.

The next question is therefore not simply whether the UK-US treaty applies. It is what the treaty may protect, what it does not protect, and which action could change the answer.

3. UK-US Tax Treaty and UK Pensions: What Articles 17 and 18 Protect for US Residents – and What They Do Not

The UK-US tax treaty is indispensable to UK pension planning for US residents. It is also widely misunderstood.

The treaty is best understood as a framework for allocating taxing rights between two jurisdictions. It determines which country has the primary right to tax particular pension events and how double taxation should be relieved. What it does not do is provide a complete answer to every pension question. Reporting obligations, transfer analysis, scheme classification, state taxation and the practical operation of US domestic law must still be considered separately. For US citizens and certain US residents, the saving clause is particularly important because it can preserve US taxing rights even where a treaty provision appears, at first glance, to offer relief.

The correct treaty analysis starts by separating the pension event being considered. Periodic pension income, lump sums, pension scheme earnings, contributions, transfers and death benefits should not be grouped together under the general phrase “the treaty covers pensions”. Articles 17 and 18 perform different functions, and neither should be treated as a universal shelter.

In broad terms, Article 17 deals with pensions, social security, annuities, alimony and child support. Article 18 deals with pension schemes, including certain questions around contributions and pension scheme earnings. Those provisions matter, but they operate within the wider treaty architecture, including Article 1 and the saving clause.

For a US resident holding UK pension assets, the practical question is not whether the treaty exists. It is which treaty article applies to the specific event, whether the saving clause changes the outcome, whether US domestic law still imposes a tax or reporting consequence, and whether the relevant position should be disclosed.

That is why a serious UK-US pension review should start with classification before strategy. The treaty answer for an untouched UK pension is not the same as the treaty answer for a lump sum. The treaty answer for a UK-to-UK transfer is not the same as the treaty answer for a transfer to Malta, Gibraltar or another third-country QROPS. The treaty answer for a non-US citizen resident in Florida may not be the same as the answer for a US citizen resident in California.

How are UK pension withdrawals taxed for US residents?

For periodic pension income, the starting point is usually residence-state taxation. HMRC’s treaty manual explains that Article 17 generally gives taxing rights over pensions to the state of residence of the beneficial owner, subject to the detailed treaty wording and relevant exceptions.

For a UK pension holder living in the United States, the United States will generally be the primary taxing jurisdiction for pension income under the treaty. However, UK PAYE remains highly relevant because pension payments are often taxed at source unless the correct treaty relief is in place. Where treaty conditions are met, applying for an NT (No Tax) PAYE code should be a priority to prevent unnecessary UK withholding and avoid lengthy reclaim procedures. This can have a significant cash-flow impact, particularly for larger pensions. Reducing UK tax at source does not eliminate the US tax analysis, but it is often one of the most important practical steps in implementing the treaty position correctly.

The distinction between UK withholding treatment and US tax treatment is important. A client can receive a UK pension payment without a US Form 1099, and the payment can still be taxable or reportable in the United States. The IRS guidance on foreign pension and annuity distributions makes clear that foreign pension income must be analysed under US rules, including the taxpayer’s cost or investment in the contract.

For higher-net-worth clients, the withdrawal decision should therefore be coordinated with the wider balance sheet. Federal tax, state tax, UK withholding, foreign tax credits, exchange rates, charitable planning, investment liquidity, concentrated equity exposure, trust distributions and family cash-flow needs should be considered together.

The wrong approach is to ask only whether the UK pension can be accessed. The better question is when, how much, in what form, in which tax year, in which state of residence, and with what evidence of pension basis.

Is the UK 25% tax-free pension lump sum tax-free in the United States?

The UK 25% pension commencement lump sum is one of the most persistent cross-border planning traps.

Before taking a pension commencement lump sum, US residents should understand how the UK-US tax treaty applies. For a detailed analysis, see our guide on Articles 17 and 18, the saving clause, HMRC guidance and IRS interpretations.

In the UK, many defined contribution pension members are accustomed to the idea that up to 25% of pension benefits can be taken as tax-free cash, subject to the relevant UK limits and scheme rules. For a US resident, that UK phrase should not be imported into the US analysis.

A UK tax-free lump sum is not automatically tax-free in the United States.

This point is supported by both HMRC and IRS materials. HMRC’s treaty manual explains that Article 17(2), which addresses lump sums from pension schemes, is not among the provisions excluded from the treaty saving clause. IRS INFO 2008-0024 reaches the same practical conclusion: the saving clause can preserve the United States’ ability to tax a US resident receiving a UK pension lump sum.

This does not mean every UK lump sum produces the same US result. The correct treatment depends on the individual’s status, pension history, contribution records, basis, treaty position, state of residence and the precise form of the distribution. But the planning principle is firm: a US resident should not take UK tax-free cash on the assumption that the United States will follow the UK treatment.

For affluent clients, the timing can be material. A seven-figure pension, a pending move between US states, a forthcoming green card decision, a business sale year, a liquidity event or a planned move away from the United States can all change the economic result. The UK availability of tax-free cash is only the beginning of the question, not the conclusion.

Contributions, pension growth and Article 18

Article 18 is another area where overconfident advice leads to poor decisions.

Article 18 deals with pension schemes, including certain rules on contributions and scheme earnings. It is relevant, particularly where an individual participated in a UK pension before moving to the United States and continues to have a connection to that scheme. But it should not be read as a broad permission slip for all post-move pension planning.

Building on the distinction between pension income and pension structures, the treaty provisions dealing with pension schemes become particularly important. These rules govern contributions, pension scheme earnings and ongoing participation in qualifying arrangements, but they do not operate in isolation. They should be analysed alongside the wider treaty framework, US domestic tax rules, reporting obligations, withdrawal planning, transfer considerations and beneficiary outcomes.

That broader framework is why historic participation and new planning must be distinguished carefully. A UK entrepreneur living in the United States can still contribute to a UK pension through employer contributions from a UK company, which can remain tax-efficient from a UK perspective. However, where a UK company employs staff in the US, establishing appropriate US retirement arrangements is generally the more suitable long-term approach.

Furthermore, inside growth is a significant advantage of retaining a UK pension while living in the United States. Properly constituted UK pension schemes are generally not taxed annually on investment growth for US purposes while assets remain within the pension. The key US tax event is usually the distribution. Contribution history and pension basis should nevertheless be documented before major withdrawals or transfers.

A proper treaty review therefore answers four questions before any action is taken:

| Treaty issue | Relevant question | Common mistake | Where to read next |

| Periodic withdrawals | Which country taxes the income, and how is withholding managed? | Assuming no UK tax means no US tax. | Article 4 decision framework |

| Lump sums | Does UK tax-free treatment survive US residence and the saving clause? | Assuming the UK 25% lump sum is automatically tax-free in the US. | Article 2 |

| Contributions | Does Article 18 apply to this contribution history? | Treating all post-move contributions as treaty-protected. | Technical tax review |

| Inside growth | Is treaty deferral available and properly documented? | Assuming all UK pension growth is automatically ignored for US purposes. | Article 3 |

| Transfers | Is the receiving scheme within the treaty framework? | Treating QROPS status as US tax approval. | Article 3 |

| Third-country schemes | Does moving the pension break the treaty assumptions? | Assuming Malta, Gibraltar or another jurisdiction inherits UK treaty treatment. | Article 3 |

This is the point at which many clients benefit from a second set of eyes before taking action. Where a UK pension is material to the family balance sheet, Harrison Brook can provide a confidential cross-border pension review at our expense, focused on treaty position, withdrawal strategy, provider suitability, reporting exposure and whether the pension should remain in the UK.

4. UK Pension Transfers and QROPS for US Residents: Why Moving a UK Pension Can Destroy the Tax and Treaty Protections That Protected It

A UK pension transfer should be treated as a high-consequence planning decision, not an administrative switch.

For US residents, the default position should usually be to keep the UK pension within the UK system unless there is a clear, documented and technically defensible reason to consider a transfer. The burden of proof sits with the transfer proposal. A transfer should improve the position after tax, reporting, investment access, regulatory permissions, currency, beneficiary planning and future residence are all considered. If it does not, the transfer should not proceed.

This is particularly important for QROPS.

A Qualifying Recognised Overseas Pension Scheme is a UK pension transfer concept. It is not a US tax classification. It is not IRS approval. It is not a guarantee of treaty protection. It is not evidence that a transfer is tax-neutral for a US resident.

A structure can be acceptable, or at least possible, under UK pension transfer rules while still being problematic under US tax, treaty or reporting rules. This is one of the defining issues in UK-US pension planning.

UK transfer permission is not the same as US tax treatment

UK pension transfer rules and US tax rules answer different questions.

The UK analysis asks whether the transfer is authorised under UK pension legislation, whether the receiving scheme satisfies the relevant conditions, whether the overseas transfer charge applies, and whether the member remains within any applicable exclusion.

The US analysis asks whether the transfer is a taxable distribution, whether the receiving scheme is recognised under the relevant treaty, whether foreign trust reporting applies, whether treaty-based positions require disclosure, whether income or gain is currently taxable, and whether the transaction creates reportable-transaction exposure.

Those are different regimes. Passing one test does not satisfy the other.

HMRC also makes clear that the published list of recognised overseas pension schemes is based on information supplied by schemes and should not be treated as a guarantee or endorsement. In practical terms, appearing on the HMRC list does not mean the scheme is appropriate for a particular member, and it certainly does not mean the IRS accepts the transfer as tax-free.

The IRS has addressed this distinction directly. IRS INFO 2011-0096 explains that a transfer from a UK pension to another UK pension can be analysed differently from a transfer to a third-country pension scheme. A third-country pension scheme, such as one established in Malta, is not a pension scheme established in the United Kingdom or the United States for purposes of the UK-US treaty definition. The IRS therefore states that such a transfer could be treated as a taxable distribution for US purposes.

That is the critical point. A transfer can preserve UK pension logic while breaking US treaty logic.

For US residents, this distinction usually makes third-country QROPS planning unattractive unless there is a very specific reason, full UK and US tax analysis, and a clear understanding of reporting and future residence consequences. For many affluent families, the cleaner solution is to retain the UK pension within an appropriate UK arrangement, improve governance and investment implementation, and coordinate withdrawals and beneficiaries within the UK-US framework.

It is worth noting that this was not always the prevailing view. For many years, particularly before the tightening of UK overseas transfer rules and increased IRS scrutiny of certain offshore pension arrangements, transferring a UK pension to a QROPS was a common recommendation for internationally mobile individuals. In some circumstances it delivered genuine benefits. However, the regulatory, tax and treaty landscape has changed significantly, and advice based on historic QROPS planning assumptions should be reviewed rather than relied upon.

Can a US resident transfer a UK pension to a QROPS?

A US resident can sometimes transfer a UK pension to a QROPS as a matter of UK pension procedure. That does not mean the transfer is sensible.

The key question is not whether a transfer form can be processed. It is whether the transfer survives the combined UK transfer-charge analysis, US tax analysis, treaty analysis, reporting analysis, investment analysis and family planning analysis.

For a US resident, the main risks are clear:

| Risk area | Planning issue | Why it matters |

| UK transfer charge | Does the 25% overseas transfer charge apply? | A transfer can be materially eroded at the point of movement. |

| Overseas transfer allowance | Does the transfer exceed the available allowance? | A charge can apply even where another exclusion appears relevant. |

| Relevant period | Will residence changes after transfer create a delayed charge? | The charge is not always a one-day test. |

| Treaty treatment | Is the receiving scheme within the UK-US treaty framework? | Third-country schemes can fall outside expected protection. |

| US tax treatment | Is the transfer treated as a distribution? | A transfer can create current US tax. |

| Reporting | Are Forms 3520, 3520-A, 8938, FBAR, Form 8833 or reportable-transaction rules engaged? | Compliance cost and penalty risk can outweigh perceived flexibility. |

| Investment implementation | Does the new structure improve or weaken portfolio access, custody and reporting? | A transfer should improve governance, not merely change jurisdiction. |

| Beneficiaries | Does the new structure improve death-benefit and succession outcomes? | Family objectives often decide the correct structure. |

Modern QROPS Risk Timeline for UK Pension Transfers and US Residents

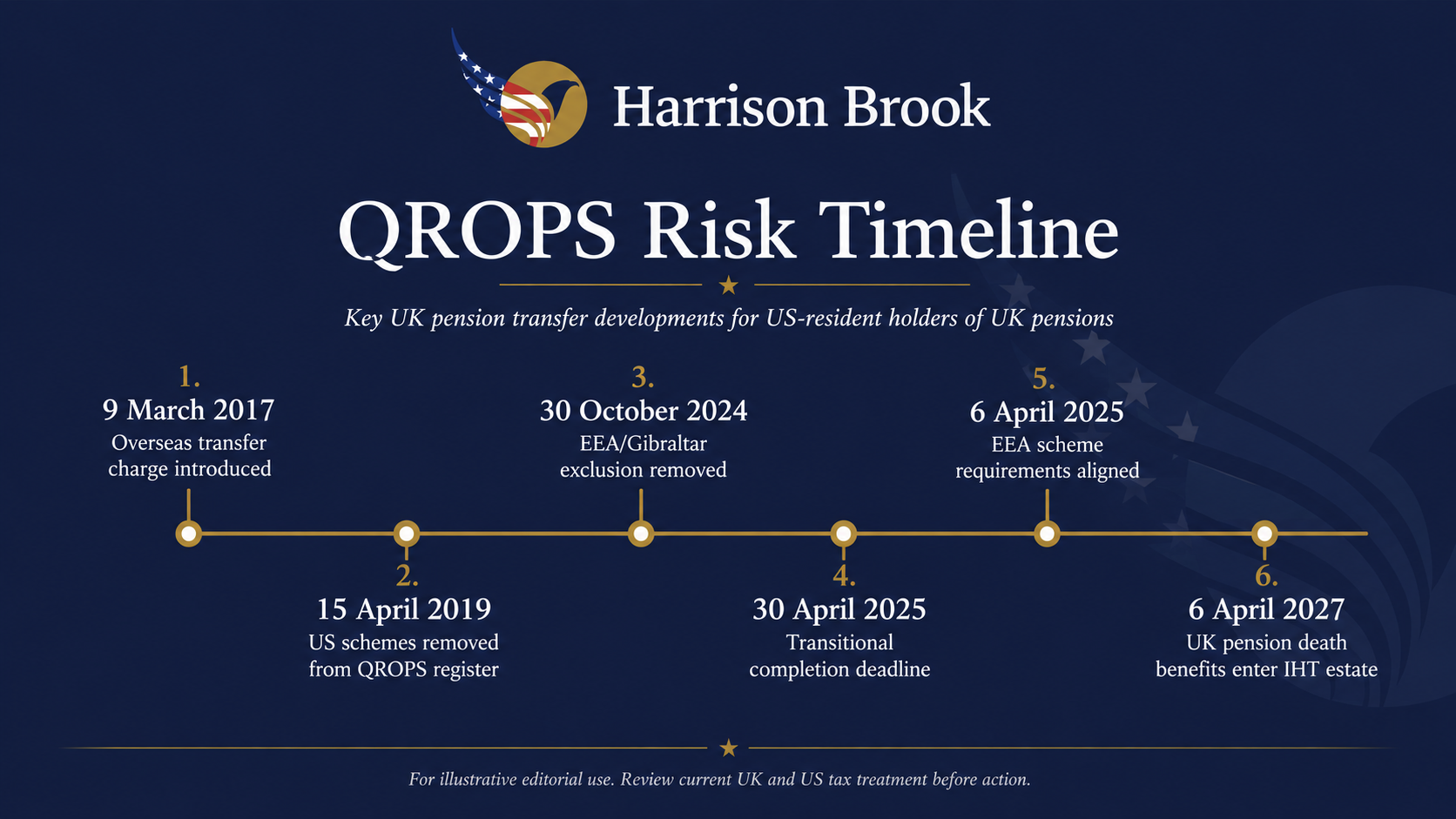

Much QROPS commentary is stale. Advice that was marginal before 2024 is often unusable after the recent UK rule changes, and several assumptions that historically drove UK-to-US pension transfer discussions are no longer available.

One of the most important developments occurred in 2019, when HMRC removed the remaining US-based pension arrangements from its published list of Qualifying Recognised Overseas Pension Schemes (QROPS). As a practical consequence, there is currently no mainstream route for transferring a UK registered pension directly into a US retirement arrangement such as a 401(k) plan or an Individual Retirement Account (IRA) while retaining QROPS status. HMRC’s published QROPS lists from 2019 onwards no longer include US schemes, and HMRC has confirmed that schemes are removed where they no longer satisfy the statutory requirements for recognised overseas pension schemes.

For UK pension holders living in the United States, this means that proposals to “move the pension into a US IRA” or “roll the UK pension into a 401(k)” should generally be treated with extreme caution. A transfer that falls outside the UK recognised overseas pension framework can trigger significant UK tax consequences, while the IRS has separately made clear that treaty provisions do not create a general tax-free rollover mechanism from a UK pension into a US-qualified retirement plan.

The position became even more relevant following the UK’s October 2024 reforms to overseas pension transfers. HMRC removed the long-standing exclusion from the Overseas Transfer Charge for transfers to QROPS established in the EEA or Gibraltar, substantially narrowing planning opportunities that had previously been used in some international pension structures.

The practical conclusion is straightforward: for most US-resident holders of UK pensions, the planning discussion should begin with whether the pension should remain within the UK pension system, rather than assuming that a transfer into a US retirement vehicle is available.

The modern timeline matters:

HMRC’s October 2024 policy paper confirms that the exclusion for transfers to QROPS established in the EEA or Gibraltar was removed for transfers made on or after 30 October 2024. It also confirms that changes to the requirements for EEA overseas pension schemes apply from 6 April 2025.

HMRC’s pensions tax manual also makes clear that the overseas transfer charge can arise after the initial transfer if the member ceases to satisfy the relevant exclusion during the relevant period. This is not merely a day-one transfer test. It is a monitoring regime that can follow the client after the pension has moved.

The overseas transfer allowance adds a further layer. HMRC states that the overseas transfer allowance is generally aligned with the lump sum and death benefit allowance, normally £1,073,100 unless an individual holds relevant protections. Where the transferred amount exceeds the available allowance, a 25% overseas transfer charge can apply to the excess even where another exclusion would otherwise have been relevant.

For high-value UK pensions, this is not a theoretical issue. A client with a £2m, £5m or larger UK pension cannot evaluate a QROPS transfer by asking whether the destination appears on a list. The review must quantify the UK transfer charge risk, overseas transfer allowance exposure, US taxable distribution risk, reporting burden, investment consequences and beneficiary outcome.

Malta QROPS, UK-US treaty planning and why older pension transfer advice should be reviewed

Malta deserves specific treatment because it appeared for years in international pension planning discussions and remains embedded in historic advice files.

The US position has changed the practical risk profile decisively.

In 2021, the United States and Malta entered into a competent authority arrangement addressing the US-Malta tax treaty. It confirmed that certain arrangements accepting non-cash contributions or contributions not limited by reference to earned personal services income are not treated as pension funds for treaty purposes. The arrangement expressly referred to Maltese personal retirement schemes under Malta’s Retirement Pensions Act of 2011.

In 2023, Treasury and the IRS issued proposed regulations identifying certain Malta personal retirement scheme transactions as listed-transaction candidates where US taxpayers claim treaty-based exclusion for inside growth or distributions. The proposal is especially relevant to UK pension holders because it expressly recognises that the UK permits tax-deferred transfers to certain QROPS, including Malta personal retirement schemes, while warning that US tax and reporting consequences can still arise.

The practical conclusion is firm. Any US resident who has transferred a UK pension to a Malta arrangement, or who has been advised to consider doing so, should have the structure reviewed. The review should cover the original transfer date, residence status at transfer, treaty position, US reporting history, income inclusion, trust reporting, reportable-transaction exposure and current exit options.

This should not be framed as “Malta is illegal” or “all QROPS are defective”. That would be imprecise. The more accurate conclusion is that many older Malta/QROPS assumptions are no longer supportable without careful evidence, and in some cases the US authorities have clearly rejected the treaty logic on which those structures relied.

Why UK-to-UK consolidation is different from a third-country transfer

Not every pension movement is a QROPS problem.

A UK-to-UK consolidation can be entirely rational where the existing provider cannot service a US-resident member properly, investment access is poor, charges are uncompetitive, beneficiary documentation is outdated, or the client needs better reporting support. However, even UK-to-UK consolidation should be reviewed before implementation where the member is US-resident.

The key distinction is that a UK-to-UK transfer keeps the pension within the UK pension system and within the treaty framework that applies to pension schemes established in the United Kingdom. It does not move the assets into a third-country arrangement whose treaty status must be analysed separately.

This distinction is not merely technical. IRS INFO 2011-0096 expressly states that a pension scheme established in a third country, such as Malta, is not a pension scheme within the meaning of Article 3(1)(o) of the UK-US treaty because it is not established in either of the two contracting states. As a result, where a UK pension is transferred to a third-country pension scheme rather than another UK pension scheme, the transfer can be treated as a distribution for US tax purposes. If treated as a distribution, the amount transferred can become taxable income under Article 17 of the treaty and under normal US worldwide income taxation principles.

For US citizens and green card holders, the consequences can be particularly severe. The IRS guidance confirms that where the individual is a US resident for treaty purposes at the time of the transfer, the transfer analysis described above applies. In practical terms, a transfer that appears tax-neutral from a UK pension perspective can be treated by the United States as a taxable pension distribution. This is one of the most important reasons why a UK-to-third-country QROPS transfer should never be evaluated solely by reference to UK pension rules or HMRC recognition status.

By contrast, a UK-to-UK transfer generally preserves the pension within the UK treaty framework and avoids introducing the additional risk that the receiving arrangement falls outside the treaty definition of a qualifying pension scheme. IRS INFO 2011-0096 therefore draws a clear distinction between UK-to-UK transfers and transfers to third-country arrangements, and that distinction should be central to any US-resident client’s planning analysis.

For many US-resident holders of UK pensions, the sensible planning sequence is therefore:

- confirm the pension type, scheme rules and provider position;

- establish the US tax and reporting classification;

- reconstruct contribution and transfer history;

- review investment access, fund selection and custody constraints;

- update beneficiary nominations and estate planning;

- consider UK-to-UK consolidation if the existing arrangement is unsuitable;

- treat QROPS or third-country transfer analysis as exceptional, not routine.

This sequence is more disciplined than starting with a receiving scheme. It also reflects the economic reality: the client is not trying to acquire a pension product. The client is trying to preserve and deploy retirement capital efficiently within a UK-US wealth structure.

Where a transfer is being considered, the review should test the UK transfer charge, overseas transfer allowance, treaty position, US reporting classification, investment access, beneficiary consequences and future residence plans before any receiving scheme is selected.

Harrison Brook offers a confidential UK-US pension review at our expense for US residents holding material UK pension assets. The purpose is not to push a transfer. It is to determine whether the pension should be retained, consolidated, drawn from, restructured or left untouched within a properly evidenced cross-border framework.

The conclusion from Sections 3 and 4 is deliberately clear. The treaty is essential, but it is not enough. QROPS status is relevant, but it is not US tax approval. A transfer can solve a provider issue while creating a tax issue. A UK pension can remain valuable precisely because it remains in the UK. For serious clients, the correct decision is not made by asking where the pension can go. It is made by asking which action preserves the best after-tax, after-reporting, after-family outcome.

5. UK Pension Access, US Tax Reporting, Investment Strategy and Estate Planning for US Residents

The technical treaty analysis is essential. It is not the whole planning exercise.

For US residents with UK pension assets, the decision is often determined by four practical questions: how the pension should be accessed, how it should be reported, how it should be invested, and how it should pass to beneficiaries. These questions are not peripheral. They are usually where the real economic result is created or lost.

UK pensions are designed primarily for UK residents. However, as more people have become internationally mobile, a number of specialist providers have developed solutions specifically for expatriates and overseas residents. Providers such as Novia Global, Invinitive, Morningstar and IFGL now offer pension and investment platforms that are better suited to clients living outside the UK, including those resident in the United States. Features can include multi-currency accounts in GBP, USD and EUR, international payment capabilities, broader investment access and administration designed for cross-border clients.

For a US resident, the quality of the provider and platform can make a significant difference to how effectively a UK pension is managed. The objective is not simply to retain the pension, but to ensure it remains practical, accessible and aligned with the client’s wider financial planning needs. Choosing the right structure can improve administration, investment flexibility and ongoing management while avoiding many of the frustrations associated with providers that are focused solely on UK-based members.

As with any cross-border pension decision, professional advice is important. Clients should seek guidance from a suitably regulated financial adviser who understands both the UK pension landscape and the practical realities of living overseas. At Harrison Brook, we offer a complimentary one-hour consultation to discuss your circumstances, review your overall objectives and determine whether we can assist with your planning.

For higher-net-worth families, the pension should be treated as part of the family’s wider wealth position rather than as a standalone retirement asset. It is not merely a retirement account. It is a tax-sensitive, treaty-relevant, investment-bearing, beneficiary-directed pool of capital sitting between two legal systems and interacting with other UK and US assets, investments, business interests and estate-planning arrangements.

The most effective outcomes are usually achieved when the pension is reviewed alongside the family’s broader financial picture under a coordinated wealth strategy. Bringing UK and US assets under a single planning framework can improve tax efficiency, investment oversight, reporting consistency, succession planning and long-term decision-making. It also helps ensure that pension decisions support, rather than conflict with, the family’s wider objectives.

The correct review therefore moves beyond the question “is the pension taxable?” and asks:

How should this pension be accessed, documented, invested and passed on within the family’s wider UK-US wealth strategy?

UK Pension Access for US Residents: A Tax, Liquidity and Family Wealth Planning Decision

The UK pension access decision should not be reduced to age, availability or provider process.

A US-resident holder of a UK pension should decide whether to draw benefits only after considering US federal tax, state tax, UK PAYE withholding, treaty relief, foreign tax credits, exchange rates, required liquidity, wider investment income, charitable planning, estate planning, family cash-flow needs, current employment status, earned income levels, Social Security benefits, UK State Pension entitlements, future retirement timing, healthcare and Medicare considerations, residency plans, and any other personal or family circumstances that may affect the overall tax and financial outcome.

This is especially important where the pension is substantial. While pensions of £3m-£5m are relatively uncommon, even a pension of around £1m can represent a significant family asset. It should not be viewed solely as a retirement-income vehicle. It can form an important part of the family’s capital reserve and succession planning. Drawing too early can accelerate tax. Drawing too late can increase exposure to UK inheritance tax under the new pension rules from 6 April 2027 and, in some cases, may also affect wider US estate tax planning. Taking a large lump sum in the wrong tax year can create avoidable inefficiency. Leaving the pension untouched without reviewing death-benefit treatment can also be an error.

The UK 25% pension commencement lump sum is the obvious example. The fact that the lump sum is available under UK pension rules does not mean it should be taken. For a US resident, the relevant question is not merely whether the UK permits tax-free cash. It is whether the United States taxes the distribution, whether state tax applies, whether there is pension basis to recover, whether the treaty position is supportable, whether disclosure is required, and whether taking the lump sum improves the family’s after-tax position.

A phased withdrawal strategy can be more rational than a large lump sum where the client needs income, wants to manage marginal tax rates, intends to move between US states, expects a future liquidity event, or wishes to coordinate withdrawals with portfolio income. Conversely, a larger withdrawal can be justified where liquidity is required for investment, family support, estate planning, debt reduction, charitable giving, or a planned departure from the United States.

There is no universal answer. But there is a correct order of analysis: tax year, treaty position, state residence, withholding, basis, currency, investment need and family objective should be assessed before benefits are taken.

US Reporting Requirements for UK Pensions: Not Just an Administrative Footnote

US reporting is one of the most underestimated issues in UK pension planning.

A UK pension can create US reporting review points even where no UK tax event has occurred. Depending on the pension structure and the taxpayer’s wider facts, the relevant analysis can include Form 8938, FBAR, Forms 3520 and 3520-A, Form 8833, and in more specialised cases, reportable transaction rules.

The point is not that every UK pension automatically requires every form. It does not. The point is that reporting should be reviewed scheme by scheme and year by year, rather than dismissed because the pension is “just a UK pension”.

Form 8938 is used by specified individuals to report specified foreign financial assets above the applicable thresholds.

For the 2026 tax year, the filing thresholds remain based on filing status and residence. Individuals living in the United States generally must file if the total value of specified foreign financial assets exceeds $50,000 on the last day of the tax year or $75,000 at any time during the year (single or married filing separately), or $100,000 on the last day of the tax year or $150,000 at any time during the year (married filing jointly).

Individuals who qualify as living abroad generally have higher thresholds: $200,000 on the last day of the tax year or $300,000 at any time during the year (single or married filing separately), and $400,000 on the last day of the tax year or $600,000 at any time during the year (married filing jointly). IRS guidance makes clear that foreign financial accounts maintained by foreign financial institutions can fall within the Form 8938 regime, subject to the relevant rules and exceptions.

FBAR reporting is separate. Filing Form 8938 does not remove an FBAR obligation where one otherwise exists. The IRS instructions to Form 8938 expressly state that Form 8938 does not relieve a taxpayer from filing FinCEN Form 114 where required.

Forms 3520 and 3520-A raise a different issue: whether the pension arrangement is treated as a foreign trust for US purposes and, if so, whether reporting relief is available. Rev. Proc. 2020-17 provides relief for certain eligible individuals with certain tax-favoured foreign retirement trusts. That relief is valuable, but it is not universal. It does not apply to every pension arrangement, and it does not eliminate all Form 8938 or FBAR considerations.

Form 8833 can also be relevant where a treaty-based return position is taken. That can arise where the taxpayer relies on the UK-US treaty to determine the treatment of pension income, lump sums, contributions, scheme earnings or residence status.

For affluent clients, the reporting issue is not just penalty avoidance. It is governance. A family with material UK pension assets should be able to explain how the pension is classified, how it is reported, what treaty position is being taken, who holds the records, and how the position changes when benefits are drawn or transferred.

This becomes particularly important after a change of adviser, a move between US states, a divorce, a green card decision, a business sale, a death in the family or a historic QROPS transfer. In each case, the pension file should be capable of review. A pension that has never been mapped properly can become a problem at precisely the point when liquidity, succession or tax certainty is most needed.

UK Pension Investment Implementation for US Residents Can Decide the Real Outcome

The investment question should not be treated as a secondary issue.

For a US-resident holder of a UK pension, the key question is not merely whether the pension remains tax-recognised. It is whether the pension can be managed properly while the member is US-resident.

Many UK providers are unwilling or unable to service US-resident clients. Others restrict investment options or offer investment ranges that remain heavily oriented toward UK investors. In some cases, pension portfolios retain significant allocations to UK equities and bonds that may no longer reflect the member’s long-term objectives, particularly where the individual now lives, earns and spends in a global or US-centric environment. Some platforms also create practical difficulties around documentation, reporting, currency management or adviser permissions.

By contrast, certain international SIPP providers offer access to thousands of investment instruments, including US equities, global equity markets, fixed income, ETFs and other diversified strategies. This can allow a US-resident member to build a pension portfolio that is more closely aligned with their wider 401(k), IRA and brokerage assets, creating a more coherent overall investment strategy across the family balance sheet.

For high-net-worth clients, the pension should be reviewed across five investment dimensions:

- Provider suitability – whether the provider can service a US-resident member properly.

- Investment access – whether the available investment universe supports the client’s objectives.

- US tax reporting – whether the investments create avoidable US tax or disclosure complexity.

- Currency exposure – whether sterling, dollar and global spending needs are aligned.

- Family liquidity – whether the pension strategy supports retirement, succession and wider asset allocation.

The treaty does not solve poor implementation. A technically retained UK pension can still be suboptimal if the portfolio is unsuitable, the provider cannot support the client, the currency exposure is unmanaged, or the family cannot obtain adequate reporting data.

This is often where UK-to-UK consolidation becomes relevant. A UK-to-UK transfer can improve provider access, investment governance and reporting support while keeping the pension inside the UK system. That is a very different proposition from transferring the pension to a third-country QROPS.

The key is discipline. The client should not transfer because a receiving scheme is available. The client should review whether the existing UK pension structure remains fit for purpose for a US-resident member. If it does not, the first planning question is usually whether a better UK-based arrangement is available.

UK Pension Beneficiaries, Death Benefits and Estate Planning for US Residents

Death planning is no longer a side issue for UK pensions.

Historically, UK pensions were often treated as highly efficient succession assets because unused pension funds could, in many cases, sit outside the member’s estate for UK inheritance tax purposes. That assumption is now changing.

HMRC’s current technical note states that from 6 April 2027, most unused pension funds and pension death benefits will be brought within the value of a deceased person’s estate for inheritance tax purposes.

For internationally mobile families, this is a material change. A UK pension should no longer be treated as a static estate-planning shelter. The analysis is now more complex because the UK has also moved away from its historic domicile-based inheritance tax framework. Under the new regime, inheritance tax exposure can arise by reference to residence-based tests and the number of years an individual has been UK resident, creating potential exposure even for individuals who are now living in the United States. As a result, a UK pension should be reviewed alongside wills, trusts, US estate tax exposure, UK inheritance tax, residence history, marital status, beneficiary residence and the family’s broader succession plan.

This is particularly important where the client has:

- a spouse or civil partner in a different tax jurisdiction;

- children resident in the United States, the UK or another country;

- a blended family or second marriage;

- minor children;

- trusts or family investment companies;

- a non-US spouse;

- US estate tax exposure;

- UK property;

- historic domicile or deemed domicile issues;

- significant illiquid assets, including business interests or carried interest;

- pension nominations that have not been reviewed since leaving the UK.

A nomination form is not an estate plan. It is one document within a wider planning architecture. In sophisticated cases, beneficiary design should be coordinated with the will, trust structure, matrimonial agreements, tax residence, domicile, liquidity planning and the family’s intended division of assets.

The 2027 UK inheritance tax reform also changes the logic of drawdown. For some clients, retaining pension assets untouched will remain rational. For others, drawing more during lifetime, rebalancing the estate, making gifts, funding life cover, supporting children, or coordinating pension withdrawals with trust planning will become more important.

The right answer depends on the client’s family structure and tax profile. But the planning principle is clear: death benefits should now be reviewed proactively, not after the pension holder has died.

Private client review checklist for US residents with UK pensions

A serious UK-US pension review should be structured around the questions that change the answer.

| Planning area | Question to answer | Why it matters |

| Residence | Is the individual US tax resident, treaty resident, dual resident, a green card holder or a US citizen? | Residence and citizenship determine the US tax, treaty and reporting framework. |

| Treaty position | Which treaty article applies to the specific pension event? | Periodic income, lump sums, contributions, inside growth and transfers are not the same issue. |

| Pension type | Is the pension a SIPP, occupational DC scheme, defined benefit scheme, historic employer arrangement or prior transferred scheme? | Scheme type affects access, reporting, transfer and beneficiary analysis. |

| Contribution history | Can employee contributions, employer contributions, transfers and prior withdrawals be reconstructed? | Basis records can affect US taxation of distributions. |

| Access strategy | Should the pension be left intact, drawn gradually, accessed through a lump sum or used for specific liquidity needs? | Withdrawal timing can change federal tax, state tax, currency and estate outcomes. |

| Transfer risk | Is any transfer UK-to-UK, UK-to-US or UK-to-third-country? | The tax and treaty consequences differ materially. |

| Reporting | Are Form 8938, FBAR, Forms 3520/3520-A, Form 8833 or reportable-transaction rules relevant? | Reporting errors can create avoidable penalties and future remediation costs. |

| Investment implementation | Can the provider service a US-resident client and support suitable investments? | Poor implementation can erode the pension’s economic value. |

| Beneficiaries | Are nominations aligned with wills, trusts, spouse position and beneficiary residence? | Pension death benefits can produce unexpected family and tax outcomes. |

| Estate exposure | How will US estate tax, UK inheritance tax and the 2027 UK pension reforms interact? | Pensions should now be reviewed as part of the taxable estate strategy. |

Where a UK pension forms a material part of the family balance sheet, Harrison Brook can provide a confidential cross-border pension review at our expense. The purpose is to establish whether the existing structure remains suitable for a US-resident member, whether reporting and treaty positions are properly understood, and whether access, investment and beneficiary planning are aligned before any irreversible step is taken.

6. UK Pension Decision Framework for US Residents: Keep, Draw, Transfer – or Pause Until the Facts Are Clear

The correct conclusion is not that every UK pension should be kept, drawn or transferred.

The correct conclusion is that each pathway should earn its place.

For US residents with UK pension assets, the four realistic options are: keep the pension in the UK, draw from it, transfer or consolidate it, or pause until the facts are clear. The last option is often underused. In complex cross-border cases, doing nothing temporarily can be the most intelligent decision where the alternative is an irreversible transfer, poorly timed withdrawal or undocumented treaty position. Where the facts are uncertain or the consequences significant, seeking advice from an experienced cross-border pensions specialist is often the most prudent course.

The decision should not be driven by product availability. It should be driven by evidence: pension type, scheme rules, residence, citizenship, treaty position, state tax, reporting classification, investment access, beneficiary planning, UK inheritance tax and future mobility.

When Keeping a UK Pension as a US Resident Is Usually the Most Sensible Option

Keeping the UK pension is often the most rational outcome for US residents.

A UK pension remains a regulated retirement structure with established rules, tax treatment, beneficiary mechanisms and provider governance. Where the scheme is suitable, the provider can service US-resident members, investment access is acceptable, reporting can be managed and beneficiary planning is current, there is usually no need to disturb the arrangement.

Retaining the UK pension can be especially appropriate where:

- the pension remains within a strong UK provider or scheme;

- the client does not need immediate liquidity;

- investment governance can be improved without leaving the UK;

- the pension is treaty-recognised and properly documented;

- reporting is manageable;

- the client expects future UK or non-US residence;

- beneficiary nominations can be coordinated with estate planning;

- a transfer would introduce UK transfer charges, US tax risk or reporting uncertainty.

The attraction of keeping the pension is not inertia. It is preservation. The client preserves the UK pension wrapper, avoids unnecessary transfer risk, maintains the pension within the UK treaty context and retains flexibility to draw benefits when the tax, family and liquidity circumstances justify it.

Keeping the pension is not always the answer. A poor provider, restricted investment access, high charges, inadequate reporting, obsolete beneficiary documents or inability to service a US-resident member can justify change. But the first question should usually be whether the pension can be improved within the UK system, not whether it can be exported.

When Drawing a UK Pension Is More Tax-Efficient Than Transferring for US Residents

Drawing from a UK pension can be more rational than transferring it.

This is particularly true where the client needs liquidity, wants to manage estate exposure, intends to fund retirement income, expects a future tax-rate change, plans to leave the United States, or wishes to coordinate pension withdrawals with wider family wealth planning.

A withdrawal is not the same as a transfer. A withdrawal accepts that the pension is being accessed and brings the relevant distribution into the tax analysis. A transfer attempts to move the pension wrapper itself. Those are different planning decisions.

Drawing can be appropriate where:

- retirement income is required;

- the pension is oversized relative to lifetime spending needs;

- UK inheritance tax exposure after 6 April 2027 is a concern;

- the client wants to reduce sterling concentration;

- a US state move creates a better withdrawal window;

- pension basis can be documented;

- the client needs capital for family support, investment or estate planning;

- phased access produces a better result than a large lump sum.

The UK 25% pension commencement lump sum should be analysed before action is taken. It should not be accessed merely because it is available. For a US resident, the UK phrase “tax-free cash” is not a US tax conclusion.

Phased withdrawals can be particularly valuable for clients who want to manage marginal tax rates, avoid unnecessary state tax, coordinate with investment income or reduce estate exposure over time. In other cases, a larger withdrawal can be justified by liquidity, succession, diversification or a planned change in residence.

The point is not that drawing is inherently better than transferring. The point is that drawing should be considered as its own strategic option. In many US-resident cases, it is a cleaner and more controllable tool than trying to move the pension to another jurisdiction.

When UK Pension Transfer Analysis Is Necessary for US Residents

Transfer analysis should always be undertaken, but only as one component of a wider pension planning and international wealth review. Analysing whether to transfer solely for the purpose of making a transfer rarely makes sense. The relevant question is not whether a transfer is available, but whether a transfer improves the client’s overall position when tax, treaty treatment, reporting, investment implementation, liquidity, succession planning and family objectives are considered together.

This can happen where the provider refuses to service US-resident members, investment access is poor, charges are materially uncompetitive, reporting support is inadequate, beneficiary documentation is unsuitable, or the client has a historic transfer structure that now needs review.

The first transfer question should usually be UK-to-UK consolidation. A properly reviewed UK-to-UK transfer can improve governance while keeping the pension within the UK pension system. It can solve practical problems without introducing the additional treaty and reporting risks associated with a third-country QROPS.

A third-country transfer should be treated as exceptional. It should not be presented as the natural solution for a US resident with a UK pension. It requires a documented UK transfer-charge analysis, overseas transfer allowance review, US tax analysis, treaty classification, reporting assessment, investment comparison and beneficiary review. As discussed earlier in this article, UK-to-third-country transfers in particular can trigger immediate US income tax consequences. Given that many UK pensions are worth hundreds of thousands, and often millions, of dollars, an adverse tax outcome can be immensely punitive and should be evaluated carefully before any transfer proceeds.

Transfer analysis is also required where the client has already transferred a UK pension offshore. Historic QROPS, Malta personal retirement schemes, Gibraltar arrangements and other overseas pension structures should be reviewed against current UK rules, IRS guidance, treaty developments and reporting history.

The practical test is simple: if the transfer does not produce a clearly superior outcome after tax, reporting, investment, regulatory and family consequences are taken into account, it should not proceed.

When pausing a UK pension transfer or withdrawal is the right answer for US residents

Pausing is often the most overlooked planning option.

In private-client work, there are many cases where the right answer is not yet available because the facts are incomplete. In those circumstances, the correct decision is to stop before taking an irreversible step.

Pausing is usually appropriate where:

- contribution records are incomplete;

- pension basis has not been reconstructed;

- US residence status is uncertain;

- a green card decision is pending;

- the client expects to move between US states;

- a UK or US tax return position is unresolved;

- prior reporting has not been reviewed;

- a business sale or liquidity event is imminent;

- divorce, remarriage or succession planning is in progress;

- the pension provider’s US servicing position is unclear;

- a prior QROPS transfer requires review;

- the client is considering a move away from the United States.

A pause is not inaction. It is controlled sequencing.

The client preserves options while the adviser team establishes the pension facts, treaty position, tax reporting profile, withdrawal alternatives, investment implementation and beneficiary plan. In many cases, pausing for proper analysis prevents a transfer or withdrawal that cannot later be unwound.

Keep / Draw / Transfer / Pause: the decision table

| Option | When it should be considered | Main risks to verify |

| Keep | The UK pension remains suitable, serviceable, reportable and aligned with family objectives. | Provider restrictions, investment access, US reporting, beneficiary nominations, 2027 UK IHT exposure. |

| Draw | The client needs liquidity, retirement income, estate reduction, currency diversification or tax-timing control. | US tax treatment, state tax, UK withholding, treaty disclosure, pension basis, lump-sum treatment. |

| Transfer | The existing arrangement is unsuitable and a better structure is justified after full UK-US analysis. | UK transfer charge, overseas transfer allowance, US taxable distribution risk, treaty status, QROPS classification, reporting. |

| Pause | The facts are incomplete, residence is uncertain, records are missing, or an irreversible decision is premature. | Lost planning window, provider limitations, unresolved reporting, upcoming tax or family events. |

The appropriate answer is usually fact-specific. For serious cross-border cases, the useful exercise is to map the pension against residence, treaty position, transfer history, reporting classification, withdrawal timing, investment access and family objectives before taking an irreversible step.

Harrison Brook offers a confidential UK-US pension review at our expense for US residents with material UK pension assets. The review is designed to identify whether the pension should be kept, consolidated, drawn from, transferred or left untouched until the facts are clearer.

The UK Pension Decision Is a Governance Question, Not a Product Question

For US residents with UK pension assets, the correct planning framework is disciplined and relatively unforgiving.

A UK pension remains a UK pension. It does not become an IRA, a 401(k) or a US-qualified retirement plan because the member lives in America. The UK-US treaty matters, but it does not answer every question. UK tax-free treatment does not automatically become US tax-free treatment. QROPS status is not IRS approval. A transfer that works under UK pension procedure can still create US tax, reporting or treaty problems.

The strongest planning outcomes usually come from resisting premature action.

The pension should first be classified. The treaty position should be established. Contribution history and basis should be reconstructed. Reporting should be reviewed. Provider suitability and investment implementation should be tested. Beneficiary nominations should be coordinated with the family’s estate plan. The 2027 UK inheritance tax changes should be integrated into the death-benefit analysis. Only then should the client decide whether to keep, draw, transfer or pause.

For many US-resident clients, retaining the pension within the UK system will remain the most rational course. In some cases, UK-to-UK consolidation will improve governance. In others, phased drawdown will be more effective than transfer. A third-country QROPS should be considered only where the facts justify it and the UK and US consequences are fully understood.

The central misconception is that the pension decision is about where the asset can be moved. It is not.

The real question is how a valuable UK retirement asset should be governed within a US tax, reporting, investment and family-wealth environment.

For internationally mobile families, entrepreneurs and executives, that question deserves more than a transfer comparison. It requires a structured private-client review, careful documentation and an adviser team that understands both sides of the Atlantic.

A UK pension held by a US resident is not a problem to be solved automatically. It is a cross-border asset to be governed properly.

If you are a US resident with significant UK pension assets and would like clarity on your options, Harrison Brook would be pleased to help. We offer a confidential review to assess the pension’s UK and US tax position, reporting obligations, investment suitability, beneficiary arrangements and transfer considerations before any irreversible decisions are made.